June 2021: Employee Retention Credit (ERC)

EMPLOYEE RETENTION CREDIT (ERC): What You Need to Know

The following communication identifies what could be a significant benefit and tax credit that could apply to many business owners who paid wages through the pandemic. The COVID-19 relief legislation passed in December 2020 enhanced the Employee Retention Credit (ERC) and more of you may qualify based on the extended and expanded rules! Note: We can calculate the credit (and potential refund), and also prepare the Amended Form 941’s necessary to claim this credit for past quarters.

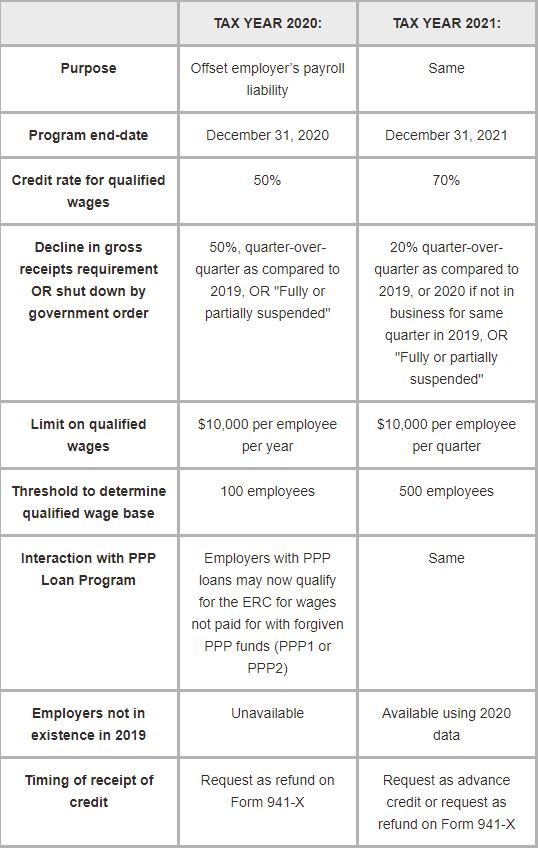

Below is a summary of some key aspects of the ERC for both 2020 and 2021 – some of which are retroactive to 2020.

Businesses starting after February 15, 2020:

A business not in existence until after February 15, 2020, is considered a Recovery Startup Business (RSB) and may be permitted to claim the ERC for Q3 and Q4 of 2021; however, the new business is subject to a maximum credit of $50,000 per quarter and must have annual receipts of less than $1 million. Note – all rules discussed below apply.

Items to Note:

Wages paid to related parties: Wages paid to an employee who is considered a “related individual” are NOT considered qualified wages for purposes of the ERC. A “related individual” is someone who has the following relationship to an owner of 50% or greater:

- A child or a descendant of a child;

- A brother, sister, stepbrother, or stepsister;

- The father or mother, or an ancestor of either; A stepfather or stepmother;

- A niece or nephew; an aunt or uncle;

- A son-in-law, daughter-in-law, father-in-law, mother-in-law, brother-in-law, or sister-in-law

- An individual who has the same principal place of abode and is a member of their household

Common ownership of businesses: Entities that have common ownership may be treated as a single employer for purposes of applying and determining the eligibility of the ERC. The common ownership rules are complex and we will analyze this for you during our initial steps of the ERC calculation.

Shut down by government order: There are specific rules which outline what is considered “fully” or “partially” shut down for purposes of the ERC.

PPP Loans and ERC: We will compare your business’s qualified period(s) for the ERC with your PPP loan covered the period to determine if the credit is worth pursuing under your specific circumstances.

Timing for claiming ERC: Credit can be claimed on Form 941-X within three years of the date the original Form 941 was filed or two years from the date you paid the tax reported on Form 941, whichever is later.

This calculation is complex. Please reach out to us for assistance if you think your business qualifies for this credit based upon the information identified above. So that we can appropriately provide you with an estimate of time and cost for us to prepare the calculation, we will request initial information from you. Upon our review of the preliminary document requests, we will correspond with you to consider the cost/benefit of the professional fees in consideration of an estimate of the credit you could receive. Every situation is different.

As always, please reach out if you have any questions on the Employer Retention Credit or if you need assistance identifying if your business is eligible for this credit for the years 2020 or 2021.

EMPLOYEE SPOTLIGHT | Christian Macleod

Christian joined the team at Soukup, Bush & Associates in June 2016. He graduated from the University of Wisconsin – Milwaukee with a Master of Science degree in Accounting. He also earned a Bachelor of Science degree in Geology and a Mathematics Certificate from the University of Wisconsin – Madison.

Christian worked for a regional public accounting firm outside of Milwaukee, Wisconsin before relocating to Fort Collins. Christian prepares both individual and business tax returns, as well as assisting with attestation services.

In his spare time, Christian enjoys hiking, golfing, skiing, and spending time with his family and his dogs.

FILING DEADLINES

SEPTEMBER 15, 2021 – Federal and state income tax returns are due for flow-through entities, including partnerships and S-Corporations if extended

SEPTEMBER 30, 2021 – Federal and state income tax returns are due for trusts if extended

OCTOBER 15, 2021 – Federal and state income tax returns are due for individual taxpayers and C-Corporations if extended

2021 ESTIMATED PAYMENT DEADLINES

SEPTEMBER 15, 2021 – 3rd quarter estimated payments for 2021 are due to the IRS and Colorado Department of Revenue